Why spend time building your own version of quicken to manage your money?

Because you are a nerd and nobody will let you tweak things just how you like it, and you want features that quicken or mint or yodlee moneycenter or ynab (you need a budget app) does not offer - like forecasting account balances for example, or you are cheap and cannot possibly spend money on something to help you track your money better.

It's been about 4 years since the original checkbook article that was somewhat popular - things have changed a bunch and I thought it would be a good time to get into it again. My thinking is I'll write about my own financial life - getting into details as much as possible, focusing on how I make decisions and plans and adjust to changes. I really enjoy financial analysis, forecasting, personal finance type conversations and writing - so it's time to explore that and try to find others that are of a similar mindset. I am married and have 5 young children, I make a normal amount of money - so this should all be interesting stuff to people that are in similar boats.

I still work for the same company as an engineer - I've moved further South and we've finalized our family of 5 little ones (no more children are planned, not that we planned any of the 5 we currently have). Things seem somewhat stable now and I still enjoy spending a few minutes each morning updating my checkbook spreadsheet while sipping on my daily cup of black coffee. My income has increased - I would say I have probably plateaued in my current position and do not expect much income increase for the time being. We have enough and are content in our lifestyle. On Saturday mornings, I typically wake up early and make chocolate chip pancakes for the kids so my wife can get some much needed rest (she still gets awakened by our 2 year old occasionally). After my wife and I eat breakfast we usually spend about 10 minutes discussing our previous budget week (runs Friday - Thursday each week). We talk about how much we spent in each category the previous week and usually go over the details for the miscellaneous category - then talk about if we were over or under budget and how things are going in the bigger picture. My wife and I both enjoy this discussion and it took us several years to get to a point where we could communicate well about money with one another. I'm a logical engineer personality, and my wife is a creative artist personality - so we do not speak each other's language naturally. My one piece of advice to engineer husbands out there, never ever send your wife a graph telling her she spent too much on groceries.

Without further ado - I'll briefly go over the current checkbook format and each tab. I'll be making a template of it available on google sheets if anyone wants to explore it further. I highly recommend building your own spreadsheet as when you build it yourself you will enjoy and understand it fully and learn a lot in the process. I completely rebuilt the spreadsheet in excel after having some issues with it crashing, then shifted it to google sheets later on and have not looked back since. I really like using google sheets - at any point my wife can look at it if she wants (she never does... but she could), and it is in the cloud and does not require a particular computer or even software to access - I can even look at it on my phone although it tends to glitch. Google sheets has come a long way over the last decade. There are a few features I could not move over (VBA programming is not quite the same on google platform) - but for the most part it works very well and any sacrifices are worth the trade-off from excel to google sheets.

This is going to be an overview - I hope to go into detail on the creation of each tab at a future date. Feel free to follow along and create your own - tweaking it as you like.

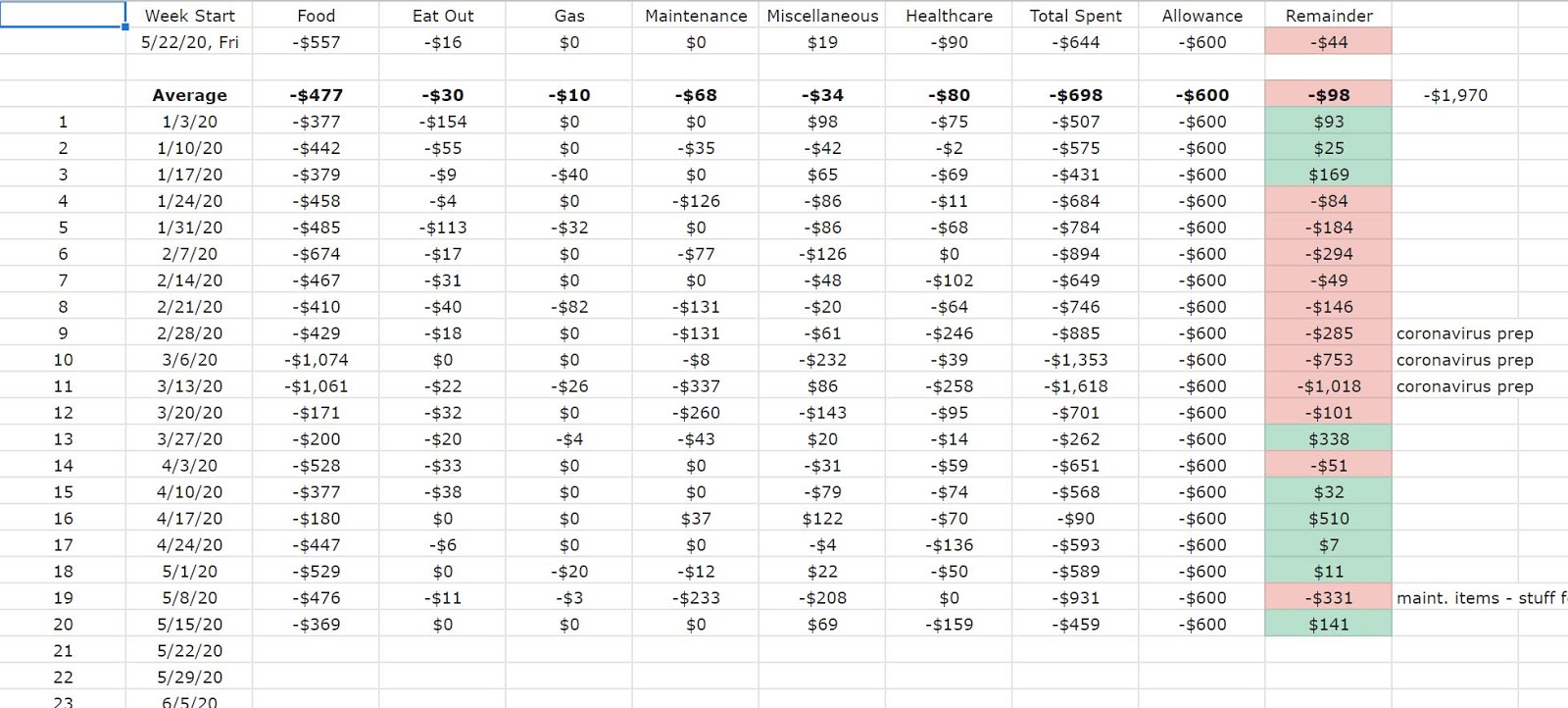

My current spreadsheet has about 14 active tabs. The most important tab by far is "Checkbook".

The Checkbook tab has an overview of each account at the top and current balances, along with the weekly summary of each category spending, net worth summary and a small section where I keep my kid's virtual bank (more on that later - it's how I teach them about money and encourage saving).

The weekly tab simply records each week and is a good place to notate anything specific for that week, and keeps track of how we're doing for the year on our spending goals.

The Net Worth tab is where I go monthly (after my mortgage is paid) to take a snapshot of my current net-worth. It's fun to track and I've really enjoyed watching how it's been impacted by the covid economy activity. It's also somewhat fun to use it to predict future net worth values - I just use the trend line formula to forecast. The slop is shown as 157 currently, which means on average my net worth increases by 157 per day. This number is slowly creeping up as my investments grow and help to boost my net worth.

The Budget tab is where I tweak our weekly/monthly/annual budget. I also maintain the store and category lists here - when we spend money at a new place I have to pop over here and add the store to the list - this helps when you want to categorize spending by store or category later and you don't have to worry about misspelling it or having multiple occurrences of the same store or category in your checkbook. A budget is pretty simple, you can see the first section is the overall budget - the 2nd section is the annual bigs where I keep track of expenses that happen once or twice annually and the 3rd section is monthly bigs where I track expenses that occur monthly. All of these automatically get thrown into the forecast tab and help to project my accounts balance into the future.

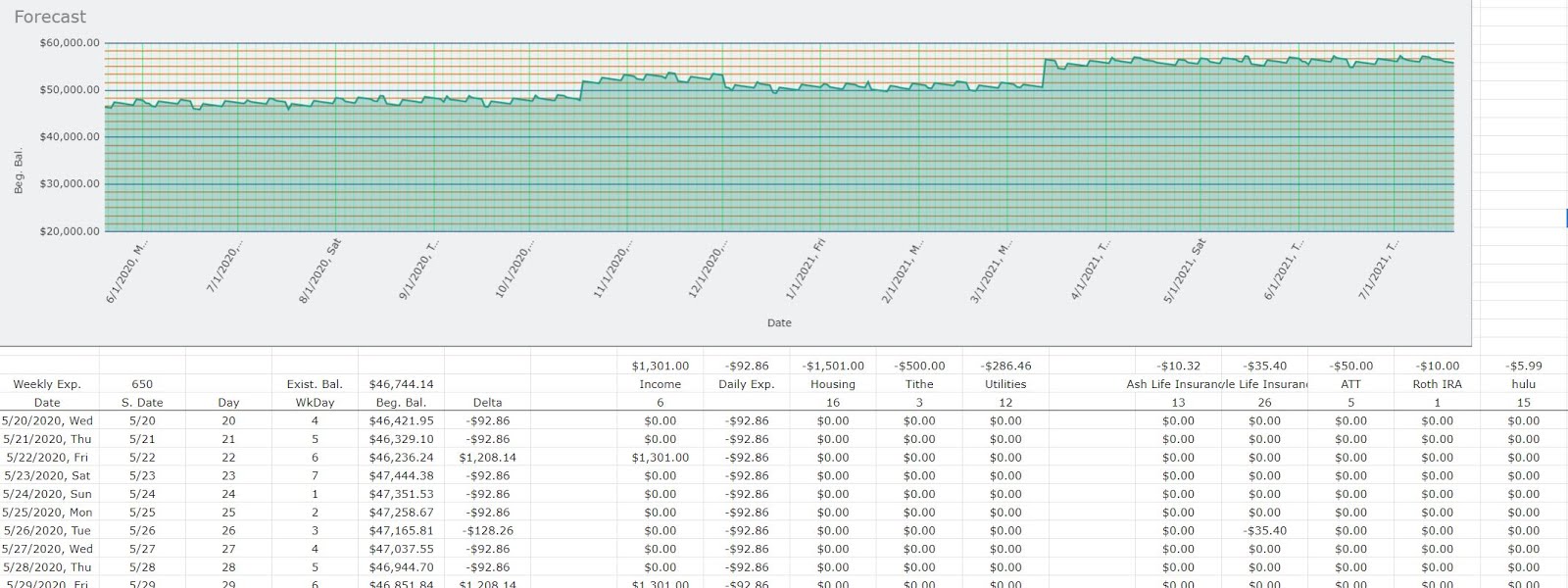

The forecast tab uses my current account balance to forecast forward with budget data as far forward as I want. It's very useful when making decisions especially when you're worried about making large payments in the future like property taxes, insurance and knowing it's okay to spend money now and still having a good margin when the property taxes are due at the end of the year.

The mortgage tab simply keeps track of where we are paying off our home, it automatically throws the current balance into the checkbook and net worth tab to report our current house equity.

The credit tab just keeps track of our credit scores. I find it very interesting how they're impacted by different things.

Bigs is where we keep track of major purchases, or other random things - when we moved my wife and I had agreed to spend around 15,000 on things we would need in our new home. I tracked it here and it's nice to be able to look back and see data on how much we spent on different things when moving here. I also track lawn care costs, vacation costs and some other random things here.

The gas tab tracks maintenance and gas costs for our vehicle. When I sold my last vehicle I added a pdf of the summary and a tally of all maintenance activities to the listing and it really impressed people and made people feel comfortable with my maintenance history and records - I would also argue people are more willing to pay a slight premium or ignore some cosmetic issues with the added documentation. It also tracks oil changes and lets me know when I need to change the oil with some conditional formatting.

The retire tab tracks my investments and helps me think through our retirement plan. It automatically grabs the current stock price on my index funds, I update the quantity of shares when I update my net worth monthly.

Stubs tracks my weekly paycheck and is a good spot to keep track of overal taxes paid annually and notice any changes to my paycheck worth investigating. I use it when checking my w2 during tax season as well.

Archive is where I move my annual transactions at the end of the year, I try to only keep 1 year of data current in my checkbook tab and keep the rest in archive. It seems to move faster that way. This is great for looking up some historic purchase my wife wonders about or if I'm curious when I bought something or for how much, I also look at trends with our category spending over time and this data is invaluable. I currently have a little over 6 years of data.

One cool thing I use this data for is creating an annual financial report every year. I record what our total income was, major expenses (I sort the checkbook from high to low), total spending categorized by store (sort checkbook by store), total spending by category (sort by category), our average weekly spending and other interesting takeaways from the year that helps us to make better future decisions with better data available.

https://docs.google.com/spreadsheets/d/1qPxQ4D_AL5tBmITaULVMHCRi6YCBjEzJS1gONK3pzCM/edit?usp=sharing